What are the different concepts related to costs? Explain the shape of the long run average cost curve according to traditional Theory. (2016 ) ( 2017 )

Concepts of Costs:- Costs concepts are used in a different way in economics as following: As these are different types of costs are..

- Money Cost

- Real Cost

- Accounting Costs

- Opportunity Costs

- Economic Costs

- Social Costs

- Private Cost

- Explicit Cost

- Implicit Cost

- Money Cost:- The Expenditure which is incurred in terms of money for the purpose of production is called Money Cost. Example :- wages paid, Taxes, Transportation Charges, Expenditure on raw materials.

- Real Cost:- The mental and physical efforts paid for producing a commodity is called real Cost. Which efforts give pain, and discomfort to the Real Owner who supplies the factor of production. It is a subjective concept.

- Accounting Cost:- Which costs are recorded in the books of accounts as depreciation and cash payments. It refers to historical costs and pocket costs.

- Opportunity Costs:- When we invest money in the form of expenditure to produce one thing, what was given up in terms of money but this money is sacrificed for next best alternatives is called Opportunity cost. Because one project is undertaken but another opportunity is foregone. It is called opportunity costs.

- Economic Costs:- Sometimes the owner supplies his own resources of production to the business otherwise his resources could earn some profit which he would have to forego. As self Employed in business for producing commodities.

- Social Costs:- Social cost is concerned with the Social cost such as Pollution and Noise. Which is borne by society like the cost, people have to bear on account of water pollution and noise pollution.

- Private Costs:- These are those costs which are borne by individual firms or individual producers as a result of their own decision making in their business operations. In short, Private costs are equal to social costs minus external costs.

- Explicit Costs:- Which sources are arranged by firms for the purpose of production, and monetary payments are made to those outsiders who supply labour services, material, fuel, transportation service, power and so on are called Explicit Costs.

- Implicit Costs:- Some inputs are self owned and self employed by the firms. The firm does not pay any payment to anyone. Rather it forgoes the opportunity to earn income from someone, Example – to whom it could sell and lease out of self owned resources is called implicit Costs.

- These types of costs almost available in every economy.

Types of costs

Explain the shape of the long run average cost curve according to traditional Theory.

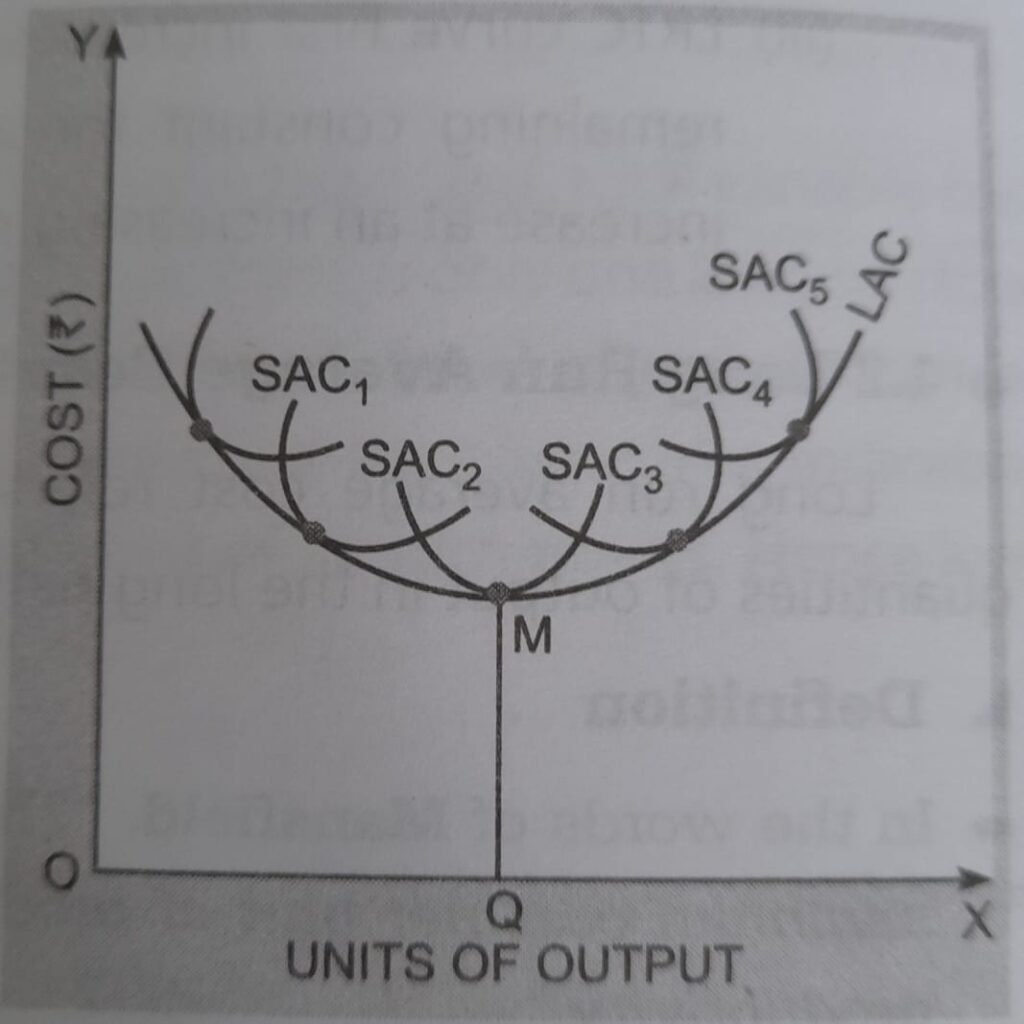

Long Run Average Cost Curve:- It reveals minimum cost per unit of production at each level of output.

It is determined by dividing long run total cost by the quantity of output produced.

As we know that each firm can use different plants in the long run. As per the demand of production he can change plant capacity as per the requirements. Each plant has its short run average cost curve with the help of which he can estimate long run average cost.

Long run average cost curve is also known by following names as

- Envelope curve

- Planning Curve

From the following figure we can analysis

Long Run Average cost Curve is tangent to each Short run average Cost curve at some point.

- To the left of minimum point M of long run average cost. This point of tangency is on the part of the short run average cost curve.

- The reason is that the slope of the long run average cost curve is reducing ( Negative ).

- As the slopes of short run average costs curve will also be negative.

- Because at the point of tangency slopes of both the curves are equal.

- On the right part of point M the point of tangency will be rising of short run average cost curves.

- It is because to the right of point ‘M’ the long run average cost curve is rising.

- At point ‘M’ long run minimum average cost and short run minimum average cost are equal to each other.

Conclusion :- Now we can understand the concept of costs and Long run average cost curves from the whole discussion. Which are analysts on the above explanation. Such different types of costs can be considered in any ongoing economy.

Important question

Relation between Average Cost and Marginal Cost

If you are tired on the way of study you can enjoy love poetry by which you can refresh your mind from the given category. types of costs